Achievement Stock photos by Vecteezy

For asset managers, double materiality is becoming an increasingly important concept when it comes to environmental, social, and governance (ESG) investing. Described by some as the ‘gold standard’ of materiality assessment, the concept is about considering and reporting on not only the material impacts of an organisation on the environment and society, but also the material impacts of a company on the climate – or any other dimension of sustainability.

Let’s take a closer look at the term’s definition, and how it affects asset management.

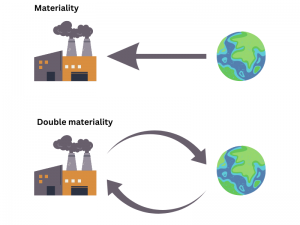

The concept of double materiality acknowledges that a company should report simultaneously on sustainability matters that are financially material in influencing business value and material to the market, the environment, and people.

Financial materiality is about economic value creation for investors and shareholders. It’s focused on how external ESG issues affect a company’s business and financial value (an ‘outside-in’ perspective).

Financial materiality is about economic value creation for investors and shareholders. It’s focused on how external ESG issues affect a company’s business and financial value (an ‘outside-in’ perspective).

The ‘operationally’ material factors are the impacts an organisation’s activities have, including impacts on communities and the environment (an ‘inside-out’ perspective). This extension on materiality is an acknowledgment that a company’s impact on the world beyond finance can be relevant and therefore worth disclosing, for reasons other than impact on a firm’s bottom line.

The concept of double materiality was introduced by the European Commission in 2019 in the context of sustainability reporting, and the need to get a full picture of a company’s impacts. The matter has been thrown into the spotlight with news of further developments from ISSB. Generally speaking, the ISSB has opted for a financial materiality approach as opposed to double materiality in its literature, but the European Commission’s Corporate Sustainability Reporting Directive (CSRD) will make it compulsory.

For asset managers, double materiality can help inform their investment decisions by providing insight into which portfolio companies are likely to be more successful over time. By focusing on companies with strong track records on both financially and operationally material ESG issues, asset managers can ensure that their investments will be more resilient in the face of changing market conditions and regulatory changes. This can help them identify potential opportunities for growth within their portfolios as well as potential risks associated with certain investments. Furthermore, by taking into account both types of ESG factors when evaluating potential investments, asset managers can make better-informed decisions about which companies are likely to outperform their peers over time.

In conclusion, double materiality is an important concept for asset managers to consider when making investment decisions related to ESG investing. Not only do financially and operationally material ESG factors have direct implications for a company’s financial performance, but they can also provide insight into which portfolio companies may be better positioned to weather changing market conditions or regulatory changes in the future.

By taking both types of ESG factors into consideration when evaluating potential investments, asset managers can make more informed decisions about which companies are likely to generate long-term returns for investors over time. With this knowledge in hand, asset managers can confidently pursue strategies that maximise returns while mitigating risk within their portfolios along that all important net zero journey.

Reach out today to discuss how SI Engage will streamline activity and data across your portfolio companies, and enhance your reporting.