Environmental Stock photos by Vecteezy

Following public consultation, the International Sustainability Standards Board (ISSB) of the IFRS Foundation has decided that global corporate sustainability disclosures will include the full range of carbon emissions; Scope 1, 2 and 3. Though due to be implemented from early 2023, there will potentially be more time to report on Scope 3 disclosures, with “relief provisions” to help work out these disclosures.

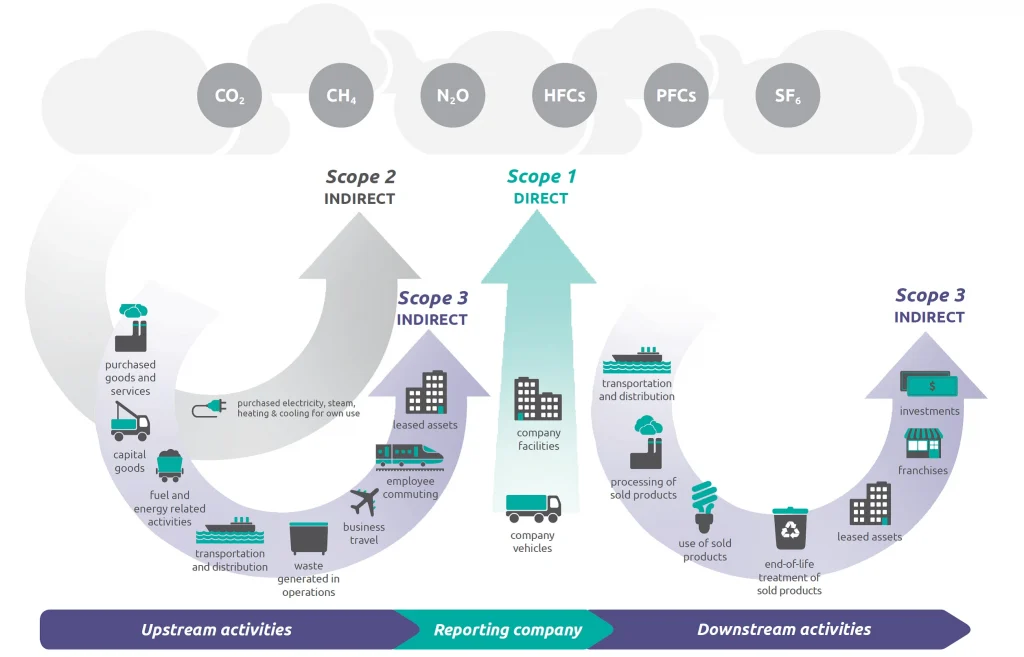

Scope 1 refers to a company’s own direct emissions, Scope 2 to indirect emissions from purchased energy, and Scope 3 to all other indirect emissions, for example through the use of the company’s products.

While asset managers generally agree that international convergence on sustainability reporting standards is needed, Scope 3 disclosures have proved contentious (read more in Morningstar’s report ESG Reporting: Asset Managers Express Divergent Views). Data collection methodology was cited as the main reason in feedback to the ISSB, but critics highlight that Scope 3, for many firms, captures the bulk of emissions and so must be included in the rules. It’s also important to note that to stand any chance of meeting net zero goals, there is no time to wait for perfect data.

The ISSB has said “its aim is to complete deliberations on the proposed standards around the end of 2022, with the view to issue the final standards as early as possible in 2023.”

The ISSB standards are expected to be used by countries like Britain, though the European Union and United States are drafting their own climate-related company disclosures. The Securities and Exchange Commission has yet to confirm its rule book for climate disclosures.